The corresponding level of authority of accounting guidelines and principles under the Generally Accepted Accounting Principles (GAAP).

I am B.com+CMA(US), working as Business Analyst for WSO. Process Optimization, Financial Analysis, & Financial Modeling

Reviewed By: Josh Pupkin

Josh has extensive experience private equity, business development, and investment banking. Josh started his career working as an investment banking analyst for Barclays before transitioning to a private equity role Neuberger Berman. Currently, Josh is an Associate in the Strategic Finance Group of Accordion Partners, a management consulting firm which advises on, executes, and implements value creation initiatives and 100 day plans for Private Equity-backed companies and their financial sponsors.

Josh graduated Magna Cum Laude from the University of Maryland, College Park with a Bachelor of Science in Finance and is currently an MBA candidate at Duke University Fuqua School of Business with a concentration in Corporate Strategy.

Last Updated: April 26, 2024 In This ArticleThe GAAP hierarchy refers to the corresponding level of authority of accounting guidelines and principles under the Generally Accepted Accounting Principles (GAAP).

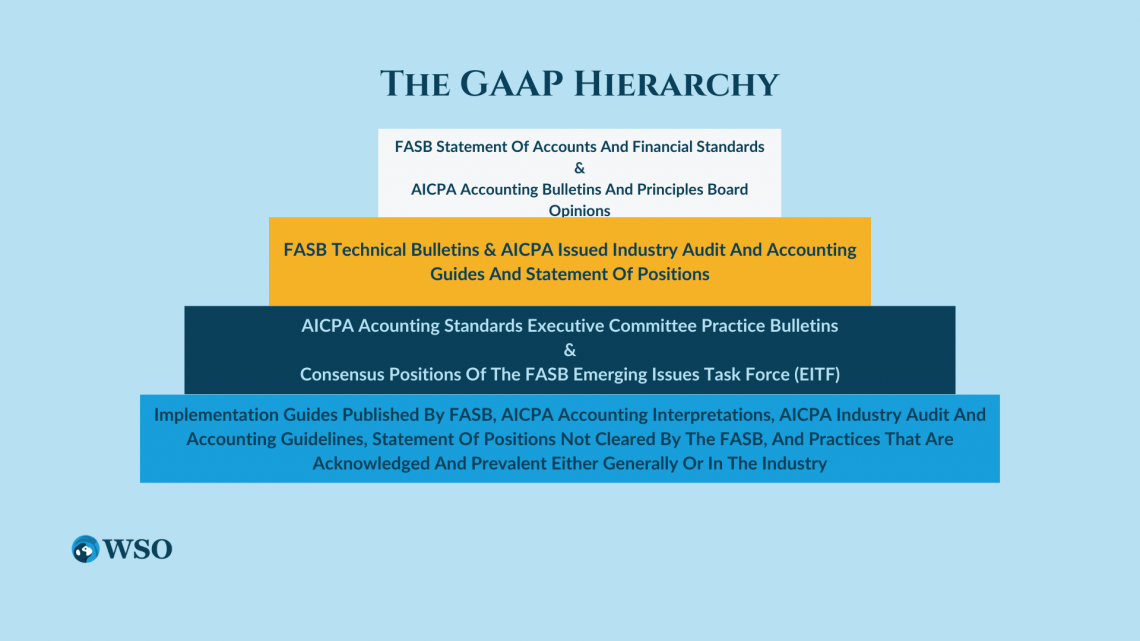

The hierarchy defines the level of authority of different accounting assertions and rulings. Therefore, when researching an accounting issue and complication, the individual should look for relevant advice at the top of the hierarchy.

The hierarchy lays down the level of authority of accounting guidelines and principles under the GAAP that regulate accounting standards in the U.S.

The highest level of the hierarchy provides broad and general rules for accounting.

It was then descending and proceeding to account for research bulletins, statements, and guidelines not cleared by the FASB.

These rules apply to any firm/company/entity required to keep accounting records.

More detailed accounting information and guidance may not apply to all organizations within the lower hierarchy.

If there is no relevant information at the top of the hierarchy, the user works down through the different order levels until the relevant pronouncement is found.

A longer explanation of the hierarchy is contained within the FASB's Statement of Accounting.

Generally accepted accounting principles (GAAP) refer to a common set of accounting standards, rules, and procedures issued by the Financial Accounting Standards Board (FASB) applicable in the United States.

These standards include the details, complexities, and legalities of business, corporate, and industrial accounting. Its compliance makes the financial reporting process transparent and systematizes and regulates assumptions, terminology, definitions, and methods.

External parties can compare financial statements issued by GAAP-compliant entities and measure the consistency, allowing quick and accurate inter-company and industrial comparisons.

Investors and stakeholders constitute a significant and essential part of any business. Their interest and confidence in the industry will determine their investment.

It's of utmost importance that an organization presents statements and reports transparently and continuously. This helps the investors and stakeholders to make sound and informed decisions.

The Financial Accounting Standards Board (FASB) was formed in 1973 as an independent nonprofit organization .

In the U.S., FASB is responsible for establishing and regulating the accounting and financial reporting standards for organizations and nonprofit firms.

In the U.S., public companies must follow GAAP when their accountants prepare and assemble financial statements. In addition, it helps the accounting world comply with general rules and guidelines.

The definitions, assumptions, and methods used across all industries for their accounting are generalized and standardized.

International Financial Reporting Standards (IFRS) are accounting standards that determine how particular types of transactions and events should be documented in financial statements.

IFRS is a more internationally recognized standard. As a result, there have been efforts in recent years to transition from GAAP reporting to IFRS.

They were developed and maintained by the International Accounting Standards Board (IASB). The IASB's purpose is to ensure that the standards are applied globally to provide stakeholders and other users of the financial statements the ability to compare the financial performances of publicly listed companies.

By employing widely agreed terminology, techniques, and procedures, Generally agreed Accounting Principles standardize and make financial reporting transparent.

Investors and other interested parties (like a board of directors) can more easily understand financial statements and compare the financial statements of one company with those of another company because of the consistent presentation of financial reports that arise from GAAP.

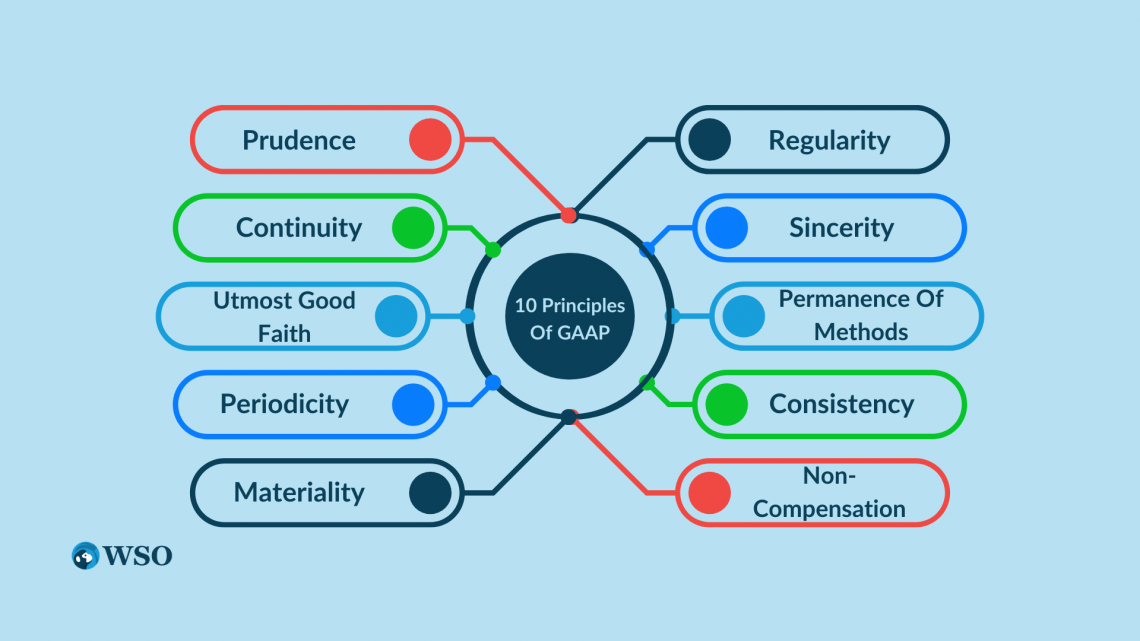

There are ten key principles that GAAP includes. They are often compared with the IFRS, which are very principle-based standards. Below are the principles:

1. Principle of Regularity

GAAP-compliant accountants stringently adhere to established rules, standards, and regulations.

2. Principle of Consistency

Consistent standards are applied throughout the financial statements and their reporting processes. This uniformity is to ensure economic comparability between periods.

Footnotes in the financial statements are used to disclose and explain the reasons behind any changes or updates in the standards.

3. Principle of Sincerity

GAAP-compliant accountants shall be committed to and for accurate and unbiased conduct. Accordingly, the accountant must strive to provide an accurate, impartial representation of the company's financial situation.

4. Principle of Permanence of Methods

Consistent procedures must be used in the preparation of all financial reports. In addition, the techniques used in financial reporting should be consistent and uniform, facilitating a comparison of the company's financial information.

5. Principle of Non-Compensation

The organization's positive or negative performance and all other aspects are reported with no consideration or prospect of compensation.

6. Principle of Prudence

Speculation does not influence the reporting of financial data. This principle emphasizes fact-based financial data representation that is not clouded by speculation.

Accountants must disclose all financial data and accounting information in financial reports.

7. Principle of Utmost Good Faith

All involved parties are assumed to be acting honestly. The Latin phrase "uberrimae fidei" is used within the insurance industry. It entails that parties remain honest in all transactions.